Market Evolution

Our perspective on what may or may not be "different this time." 1

Market history can provide useful context for investors. Today, markets are digesting the massive AI buildout and the largest private companies in the world going public. These seismic shifts may lead investors to look to the past for context. Is this 1996 or 1999? Or perhaps 2007 vs 2013? Or even the roaring 1920’s and what followed 100 years ago. We believe it’s important to be students of market history, yet not become blinded by history. Today’s market structure differs in meaningful ways from prior points in history.

To blindly follow history is searching for past precedents and operating under the assumption that the market of today is structurally identical to the market of 1929, 1974, or even 1999. We believe the underlying complexion, participant base, technological infrastructure, and fundamental math of corporate America have evolved profoundly, and the market of today is not structurally identical to the markets of 1929, 1974 or 1999. To build a robust, forward-looking investment framework, we consider four pillars that may have structurally altered how the current market behaves.

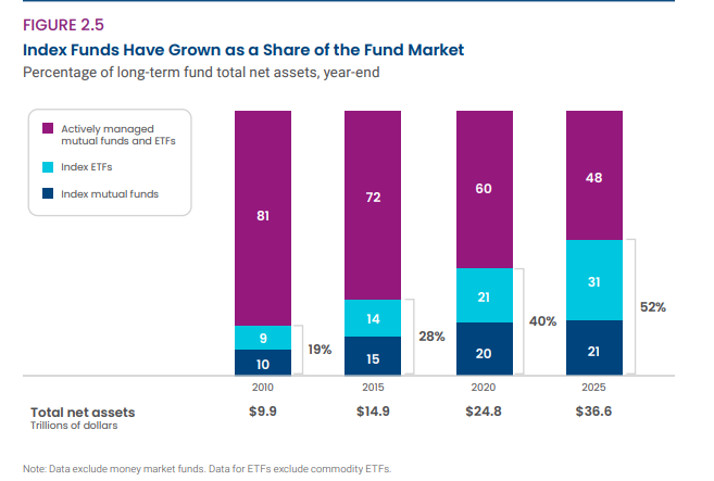

Pillar 1: The Rise of Institutional and Passive Ownership

The equity market historically included a larger share of active participants such as individual retail stock pickers and active mutual fund managers. Today, the ownership base of public equities has experienced a material shift. A large and relatively passive institutional base (such as BlackRock, Vanguard, and State Street) now represent a meaningful share of ownership in many major public companies. These institutions represent a perpetual pool of long-term capital tied to broader index structures. As the chart below shows, index ownership within mutual funds and ETF’s is now the majority of long-term fund total net assets.

Source: https://www.icifactbook.org/pdf/2026-factbook.pdf

Pillar 2: Algorithmic Trading and Market Velocity

When looking at events like the Great Depression or the stagflation corrections of the 1970s, market movements unfolded over weeks, months, or years. The average trade required a person to hear the news via newspaper, radio, or television. Then that person needed to make a conscious cognitive decision, physically execute a ticket, or pick up the telephone.

Today, a significant portion of trading activity is automated. According to Professor of Finance at FIU Suchismita Mishra, about 70% of the comprehensive trading volume in the US stock market is initiated through algorithmic trading.

These models operate on absolute mathematical parameters, executing complex block trades in milliseconds based on quantitative factors distinct from traditional human emotion. This high speed, algorithmic trading can lead to near immediate pricing of new information. If the 2020’s are any indication, we may live in a new era of faster market corrections and recoveries compared to past market cycles, even though there can be no assurance that this pattern will continue or that future market cycles will resemble recent ones.

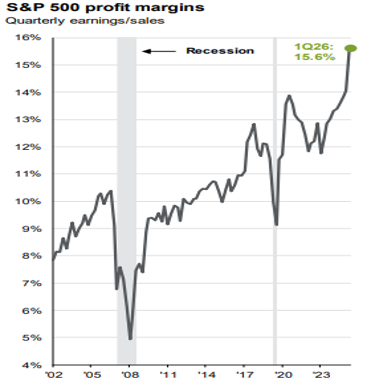

Pillar 3: Structural Corporate Efficiency (Margins and ARR)

One common argument for market overvaluation is that current price-to-earnings (P/E) multiples are above their long-term historical means. At the same time, investors should consider whether changes in business models, sector composition, interest rates, tax policy, globalization, and profitability may affect the interpretation of historical valuation comparisons. As seen in the chart below, S&P 500 company profit margins have pushed structurally higher in the 21st century vs. in earlier periods.

Part of this may be attributed to how corporations earn their revenue. Twenty years ago, much of corporate revenue was purely transactional. Today, a massive portion of enterprise revenue has shifted to high-margin, Annual Recurring Revenue (ARR) formats. A business with a higher profit margin and more predictable, recurring revenue may command a higher valuation multiple than a low-margin, transactional manufacturing business of the past. However, valuation multiples remain sensitive to interest rates, growth expectations, competition, execution risk, and changes in investor sentiment.

As we look ahead, AI may affect profit margins via capital expenditure, productivity, and operating cash flow. The ultimate effect is uncertain and may vary significantly by company or sector. This chapter of the market is being written in real time.

Source: https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/guide-to-the-markets/

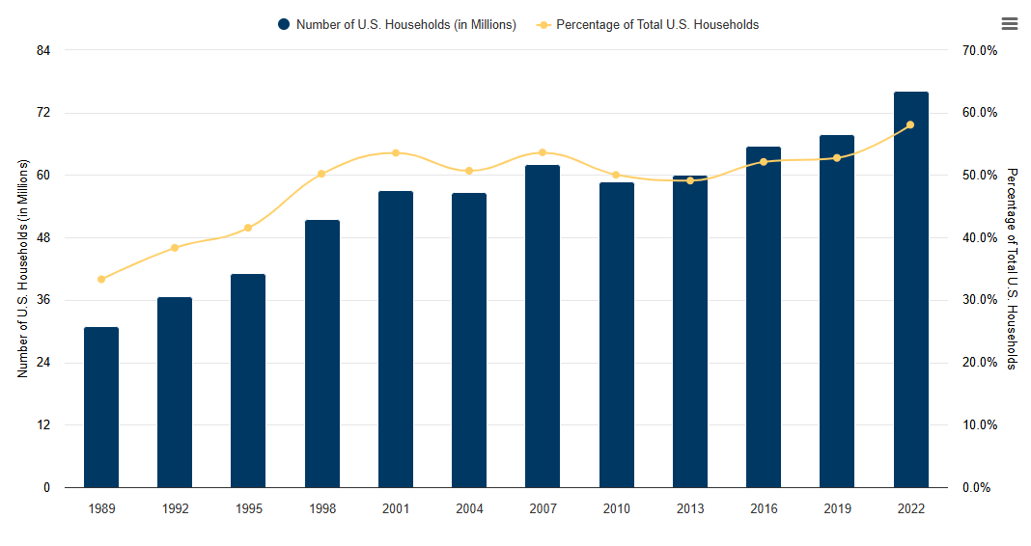

Pillar 4: The Asset Mix Realignment (Household Ownership)

The final structural shift is demographic. If you look at the composition of wealth in U.S. households generations ago, individual wealth was heavily concentrated in tangible, illiquid assets such as residential real estate and bank deposits. The composition of U.S. household wealth has changed over time, and access to public markets has broadened through lower-cost brokerage platforms, index ETFs and employer retirement plans such as 401(k) plans. As the chart below illustrates, the last 35 years have experienced a transformational change. Today, a majority of US households are stock and bond owners, over double from just 35 years ago. Broader household participation may affect market structure, but it also means that more households are exposed to market volatility and potential investment losses.

The Guardrail: Why We Remain Students of History

If the structural math and plumbing of the market are so different, why study history at all? We remain students of history because we believe human psychology is immutable. The tools may evolve from ticker tape and chalkboards to fiber-optic algorithmic servers, but underlying human cognitive biases remain the same. Our conviction is that primal impulses of greed and fear remain constant, and risk appetite and behavioral biases will continue to affect markets.

The value of studying history is not found in expecting history to perfectly repeat. The value of history lies in studying how humans respond to systemic leverage, how crowds behave during speculative asset bubbles, and how markets react to policy decisions. Historical comparisons provide context but are not a forecast or guarantee of future market outcomes.

The Bottom Line:

As we evaluate modern markets and construct forward frameworks, we honor the past but are not blinded by it. We look at historical cycles to deep-dive into human behavior, but always cross-reference those lessons with the current landscape. We encourage all investors to be students of history, but caution against solely relying on history, or you may miss the evolution right in front of you.

If you or someone you know are questioning how current events may impact their investment plan, please reach out to us today.

1 Important information: This commentary is for informational and educational purposes only and should not be construed as individualized investment advice or a recommendation to buy, sell, or hold any security or strategy. Investing involves risk, including the possible loss of principal. Past market environments and historical observations do not predict future results, and forward-looking statements are based on assumptions that may change without notice. Data and charts are from the cited third-party sources and should be reviewed for continued accuracy before use.

All investing involves risk, including the possible loss of principal. Nothing contained herein should be construed as individualized advice and is for informational purposes only. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client's investment portfolio. Past performance is no guarantee of future performance. Seven Springs Wealth Group is an investment adviser registered with the US Securities and Exchange Commission (SEC). Registration does not imply any level of skill or training. For a complete discussion of Seven Spring Wealth Group’s services and fees, you should carefully review the firm’s disclosure brochure available at www.adviserinfo.sec.gov